In 2025, the Federal Reserve’s decision to cut interest rates is a pivotal moment for the economy, impacting everything from your mortgage payments to your investment portfolio. With inflation cooling and labor market dynamics shifting, the Fed’s monetary policy adjustments, led by Chair Jerome Powell, aim to balance growth and stability. This comprehensive guide explores what Fed rate cuts mean, their historical context, and how they affect mortgages, stocks, savings, and more. Whether you’re a borrower, investor, or saver, understanding these changes is crucial for making informed financial decisions.

Understanding Federal Reserve Interest Rate Cuts

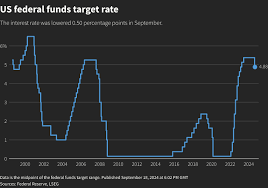

What is the Federal Funds Rate?

The federal funds rate is the benchmark interest rate at which banks lend to each other overnight. Set by the Federal Open Market Committee (FOMC), this rate influences borrowing costs across the economy, from consumer loans to corporate bonds. When the Fed cuts rates, it lowers the cost of borrowing, encouraging spending and investment to stimulate economic growth.

Why Does the Fed Cut Rates?

Rate cuts typically occur when the Fed aims to:

- Stimulate the economy: Lower rates encourage borrowing and spending, boosting economic activity during slowdowns.

- Control inflation: With inflation trending toward the Fed’s 2% target in 2025, rate cuts can prevent deflationary pressures.

- Support employment: Easing monetary policy can bolster job creation if labor market data, like non-farm payrolls, shows weakness.

In September 2025, the Fed’s dovish stance reflects cooling inflation and a focus on sustaining growth amid global uncertainties. For example, a 50-basis-point cut could lower the federal funds rate to a range of 4.25%-4.5%, signaling a proactive approach to economic challenges.

Historical Impact of Fed Rate Cuts on the Economy

Lessons from Past Rate Cut Cycles

Historically, Fed rate cuts have had mixed effects. During the 2008 financial crisis, aggressive rate reductions paired with quantitative easing stabilized markets but led to prolonged low yields. In 2019, pre-COVID cuts boosted stock markets but didn’t prevent a recession. Data from the St. Louis Fed shows that S&P 500 returns often rise 10-15% in the year following initial rate cuts, though volatility can spike if recession fears persist.

Fed Rate Cuts Near All-Time Market Highs

In 2025, markets are near record highs, raising questions about rate cut impacts. Historically, cuts during bull markets (e.g., 1995) have extended rallies, particularly in growth stocks. However, overvaluation risks in sectors like technology could lead to corrections if investor sentiment shifts. Monitoring treasury yields and market volatility is key during this period.

How Fed Rate Cuts Affect Mortgage Rates and Borrowing Costs

Pros for Borrowers: Lower Loans and Credit Cards

Rate cuts directly lower borrowing costs. For homeowners, a drop in the federal funds rate often reduces mortgage rates. For instance, a 30-year fixed mortgage rate might fall from 6.5% to 6% after a 50-basis-point cut, saving borrowers thousands over the loan’s life. Similarly, credit card APRs, tied to the prime rate, could decrease, easing debt burdens. According to the Mortgage Bankers Association, refinancing applications typically surge 20-30% after rate cuts.

What Happens to Prime Rates After a Cut?

The prime rate, used by banks for consumer loans, moves in lockstep with the federal funds rate. If the Fed cuts rates by 50 basis points, the prime rate might drop from 8% to 7.5%, reducing costs for home equity loans and personal loans. This makes 2025 a potentially favorable year for refinancing or securing new loans.

Fed Rate Cuts and the Stock Market: Opportunities and Risks

Top Stocks to Watch During Rate Cuts

Lower interest rates benefit growth-oriented sectors:

- Technology: Companies like Apple and Microsoft thrive as borrowing costs drop, enabling expansion.

- Consumer Discretionary: Retail and e-commerce stocks, such as Amazon, often rally due to increased consumer spending.

- Real Estate: REITs like Vanguard Real Estate ETF (VNQ) gain as mortgage rates decline.

However, cyclical sectors like financials may lag, as banks earn less on interest margins. Diversifying across sectors is a prudent strategy.

Impact on S&P 500 Performance

Historical data suggests the S&P 500 often performs well post-rate cuts, with average returns of 12% in the first year, per Bloomberg analysis. However, near all-time highs in 2025, investors should watch for overbought conditions. Defensive stocks, like those in healthcare or utilities, can provide stability if volatility rises.

Effects of Fed Rate Cuts on Savings, Gold, and Silver

Challenges for Savers and High-Yield Accounts

Rate cuts are less favorable for savers. High-yield savings accounts and CDs, which offered 5% APYs in 2024, may drop to 4% or lower in 2025. This squeezes returns for retirees and conservative investors. Consider locking in rates with longer-term CDs before further cuts take effect.

How Rate Cuts Influence Precious Metals Prices

Gold and silver often rally during rate-cutting cycles due to lower real interest rates and a weaker dollar. In 2025, gold prices could climb toward $2,800/oz if the Fed signals sustained easing, as seen in past cycles. Silver, more volatile, may outperform gold in percentage gains, making it attractive for speculative investors.

Fed Rate Cuts 2025 Predictions and Portfolio Strategies

Expected Basis Point Cuts This Year

Analysts expect the Fed to cut rates by 75-100 basis points in 2025, potentially lowering the federal funds rate to 3.75%-4% by year-end, based on CME FedWatch Tool projections. FOMC meetings in September and December 2025 will be critical, with Chair Powell’s commentary shaping market expectations. Watch for labor market data and core inflation trends as key drivers.

How to Prepare Your Investments for Rate Easing

To navigate rate cuts:

- Diversify investments: Allocate across equities, bonds, and precious metals to hedge risks.

- Focus on growth stocks: Tech and consumer discretionary sectors often outperform.

- Consider bonds: Treasury yields may dip, making intermediate-term bonds attractive.

- Monitor real estate: Lower mortgage rates could boost housing demand, benefiting REITs.

- Stay liquid: Keep cash reserves for opportunities if markets correct.

FAQs on Fed Rate Cuts

What Do Fed Rate Cuts Mean for Inflation?

Rate cuts can rekindle inflation if stimulus overshoots, but with 2025 forecasts showing inflation near 2%, the Fed’s cuts aim to maintain balance. Core inflation metrics, like PCE, will guide future decisions.

Will Fed Cuts Cause a Recession?

While rate cuts often signal economic concerns, they’re designed to prevent recessions. In 2025, recession risks remain low (25-30% probability, per Goldman Sachs), but global uncertainties could amplify risks if cuts are mistimed.